Component Depreciation Method: IAS 16 Guide with Worked Examples

IAS 16 component depreciation explained: how to identify significant components, assign separate useful lives, and build compliant depreciation schedules. Practical GCC examples.

ACA | FMVA® | 19 Years in Finance

Treat a USD 5 million commercial building as a single asset over 40 years and your annual depreciation charge is USD 125,000. Apply IAS 16 component accounting to the same building and the number is USD 238,333. That is a USD 113,333 difference: every year, on a single property.

Componentisation is not a technicality. It is one of the most commonly flagged IAS 16 non-compliance items in GCC audits. Finance teams know the rule exists. The problem is the application: which parts count as significant, how do you assign lives, and what happens when a component needs replacing before its estimated end date?

This post covers the component depreciation method in full, with the Bahrain building numbers worked through completely.

Table of Contents

- What the Component Depreciation Method Requires Under IAS 16

- When You Must Componentise: The Significance Test

- Identifying Significant Components: A Decision Framework

- Building a Component Depreciation Schedule: Step by Step

- Worked Example: Commercial Building in Bahrain

- Component Replacement: Derecognition Before End of Life

- Component Method vs Single Asset: The P&L Impact

- IAS 16 Disclosure Requirements

- Common Mistakes and Audit Findings in GCC Practice

- FAQ

1. What the Component Depreciation Method Requires Under IAS 16 {#definition}

IAS 16.43 states: "Each part of an item of property, plant and equipment with a cost that is significant in relation to the total cost of the item shall be depreciated separately."

That sentence is mandatory. When an asset has significant parts with materially different useful lives, you do not get to choose whether to componentise. You must.

The practical translation: instead of one depreciation schedule for the whole asset, you build separate schedules for each significant component. Each component has its own cost, its own useful life, and its own annual charge. You sum the individual charges to get total depreciation for the period.

IAS 16.47 adds the corollary: the remainder of the asset: the parts not individually significant: is grouped together as a residual component and depreciated as a single amount. The whole asset is always accounted for, even when only some parts are explicitly separated. The full IAS 16 standard is at ifrs.org.

2. When You Must Componentise: The Significance Test {#significance}

IAS 16 does not give you a number. "Significant in relation to the total cost" is a judgement, not a threshold. Standard-setters left it that way deliberately: a fixed percentage would be gamed.

In practice, most entities that have thought through their accounting policy apply 10-15% of total asset cost as the internal trigger for treating a part as significant. Below that threshold, the part is aggregated into the residual component. Above it, it is separated.

Three conditions should all be present before you separate a component:

| Condition | What to Assess |

|---|---|

| Physical separability | Can the part be replaced independently without affecting the rest? |

| Materially different useful life | Does the part's life differ from the overall asset by more than a few years? |

| Cost significance | Does the part exceed your documented threshold (typically 10-15% of asset cost)? |

Document your significance threshold as an accounting policy. Auditors will ask for it. If you have applied componentisation to some assets but not others of a similar type, the policy is what justifies the difference.

One practical point: the significance test applies at initial recognition. When you first capitalise the building, you componentise based on the initial cost allocation. If you add a major improvement later, assess whether that addition creates new significant components.

3. Identifying Significant Components: A Decision Framework {#identify}

For a commercial building, the starting point is the original cost breakdown from the quantity surveyor's report or contractor's valuation. You are looking for distinct physical systems that have independent replacement cycles.

Common significant components for commercial buildings:

| Component | Typical Useful Life | Why Significant |

|---|---|---|

| Structure (frame, slabs, foundations) | 40-60 years | Largest single cost element; long-lived |

| Roof (covering, insulation, waterproofing) | 15-25 years | Replaced independently on a maintenance cycle |

| HVAC system (chillers, ducts, controls) | 12-20 years | Major plant replaced on technology and wear cycles |

| Lifts and escalators | 20-30 years | Separately maintained and replaced; regulated safety cycles |

| Interior fit-out (partitions, finishes, services) | 8-15 years | Replaced on lease renewal or business change |

| External cladding / facades | 20-35 years | Significant cost, replaced independently of structure |

For manufacturing and industrial assets, the equivalent breakdown includes: structural steel frame, process equipment, electrical systems, control and instrumentation, and roofing.

What to do when the original cost allocation is unavailable: If you are componentising an existing asset for the first time and the contractor's cost breakdown no longer exists, use a professional valuation or engineer's apportionment to establish the split. Retrospective componentisation is permitted; the IAS 8 treatment depends on whether the change is voluntary (change in accounting policy, typically applied retrospectively) or a correction of prior error.

The residual component captures everything not explicitly separated. It is depreciated over the overall asset's remaining useful life.

4. Building a Component Depreciation Schedule: Step by Step {#steps}

Step 1: List all components and their allocated costs. Use the cost breakdown to assign a cost to each significant component. The sum of all component costs must equal the total asset cost.

Step 2: Assign useful lives. Each component gets its own estimated useful life based on physical characteristics, maintenance contracts, and industry norms. Useful lives are estimates: document the basis for each.

Step 3: Assign depreciation methods. Each component can have a different method (IAS 16.62). In practice, straight-line is used for most building components. Where usage drives wear on a component: a manufacturing process unit, for instance: units of production could apply to that component alone.

Step 4: Calculate annual depreciation per component. Straight-line: cost divided by useful life. No residual value is typically assumed for building components (the structure itself may have a residual, but fit-out and services generally reach nil).

Step 5: Sum to get total asset depreciation. The total annual charge equals the sum of all component annual charges. This feeds into the P&L and the asset register.

Step 6: Annual review. IAS 16.61 requires review of each component's useful life, residual value, and depreciation method at every year end. Where estimates change, apply the revision prospectively.

5. Worked Example: Commercial Building in Bahrain {#worked-example}

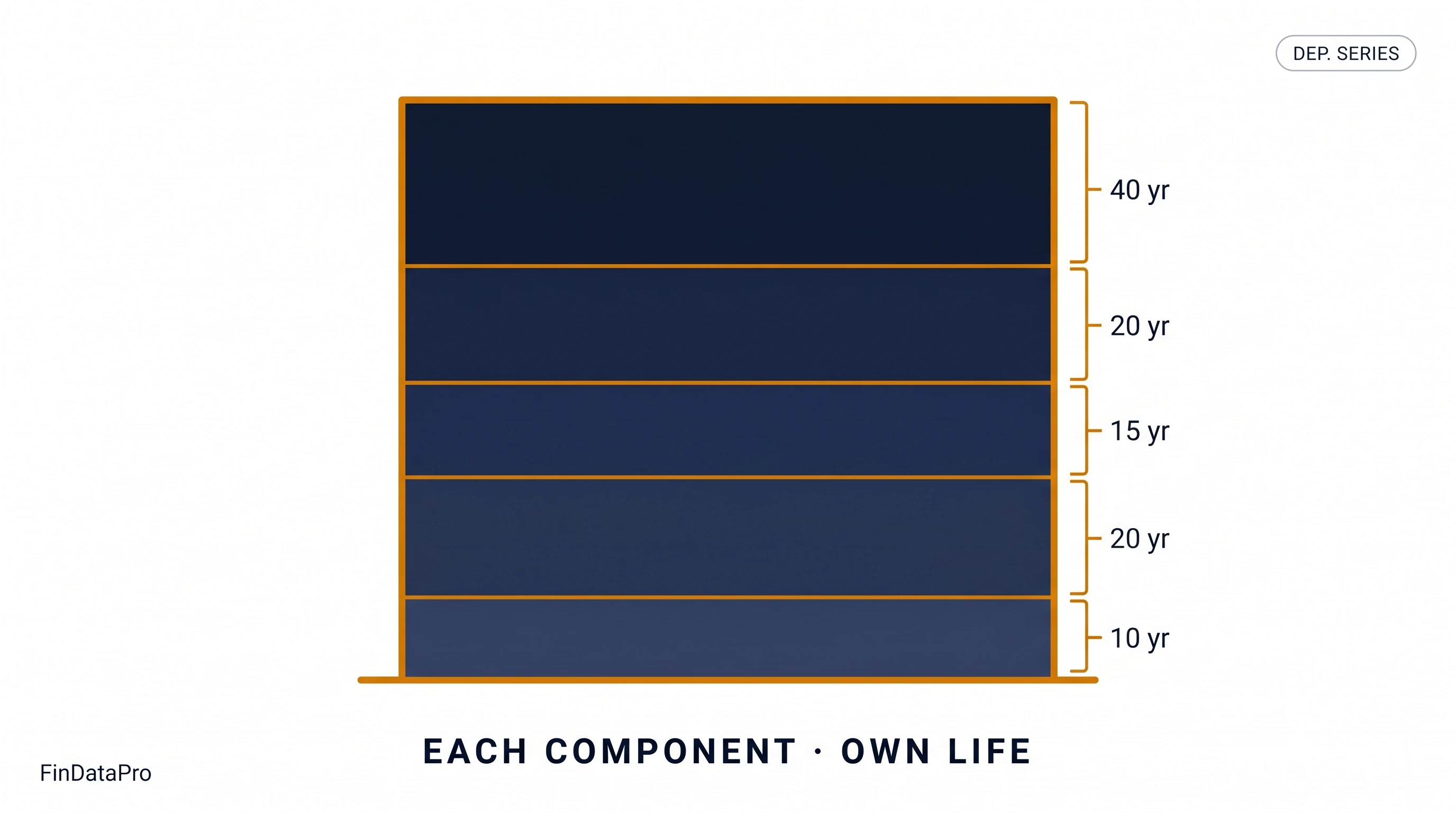

Asset: Commercial office building, Manama, Bahrain Total cost: USD 5,000,000 Ownership: GCC listed entity reporting under IFRS (CBB rules)

Component breakdown and annual depreciation (straight-line, nil residual per component):

| Component | Cost (USD) | % of Total | Useful Life (Years) | Annual Depreciation (USD) |

|---|---|---|---|---|

| Structure | 2,500,000 | 50% | 40 | 62,500 |

| Roof | 750,000 | 15% | 20 | 37,500 |

| HVAC System | 500,000 | 10% | 15 | 33,333 |

| Lifts / Elevators | 400,000 | 8% | 20 | 20,000 |

| Interior Fit-Out | 850,000 | 17% | 10 | 85,000 |

| Total | 5,000,000 | 100% | : | 238,333 |

For comparison: single asset approach (40 years):

USD 5,000,000 ÷ 40 = USD 125,000 per year

The component method produces USD 238,333 per year: 91% higher than the single-asset approach.

This is not an aggressive accounting position. It is the IAS 16-compliant position. The single-asset approach with a 40-year life misrepresents the economic reality: the fit-out will need replacing in Year 10, the HVAC in Year 15, and the roof in Year 20. Charging USD 125,000 every year smooths over those replacement cycles entirely.

Years 1-10 depreciation schedule (showing how the charge steps up over time):

For the first 10 years, all five components are being depreciated simultaneously. The total charge is USD 238,333 per year throughout this period.

At Year 10: The interior fit-out reaches the end of its estimated life. If replaced immediately, the old fit-out is derecognised (see Section 6) and a new fit-out is capitalised. If no replacement occurs: perhaps the building is being redeveloped: the fit-out component is fully depreciated and the total charge drops to:

62,500 + 37,500 + 33,333 + 20,000 = USD 153,333 per year

This step-down in depreciation charge corresponds directly to the physical reality of a fully expensed component with no replacement yet planned. Single-asset accounting would still be charging USD 125,000 against a 40-year asset with a fictitiously clean NBV.

6. Component Replacement: Derecognition Before End of Life {#derecognition}

Suppose at Year 8, the HVAC system develops a fundamental fault and requires full replacement. The original estimate was 15 years. Eight years of use remain.

Step 1: Calculate remaining NBV of old HVAC:

| Item | USD |

|---|---|

| Original HVAC cost | 500,000 |

| Accumulated depreciation (8 × 33,333) | 266,667 |

| Remaining net book value | 233,333 |

Step 2: Derecognise the old component:

Remove USD 500,000 from gross cost. Remove USD 266,667 from accumulated depreciation. The remaining USD 233,333 NBV is recognised as a loss in profit or loss in Year 8. This is not an error: it is the accounting consequence of a component failing earlier than estimated.

Step 3: Capitalise the replacement:

The new HVAC system costs USD 580,000 (technology has advanced; a like-for-like replacement is more expensive). Estimate its useful life: 15 years. Annual depreciation from Year 9: USD 580,000 ÷ 15 = USD 38,667.

P&L impact in Year 8:

| Item | USD |

|---|---|

| Depreciation on all components (normal) | 238,333 |

| Loss on derecognition of old HVAC | 233,333 |

| Total charge in Year 8 | 471,666 |

This spike in Year 8 is the consequence of the original useful life estimate being wrong. Single-asset accounting would have continued charging USD 125,000 without any P&L recognition of the failed component: then recognised the full replacement cost as maintenance expense or capitalised it without removing the old value, both of which misstate the balance sheet.

The derecognition approach forces transparency. The P&L in Year 8 shows what actually happened to the asset.

DepreciationLab handles component derecognition automatically.

When you replace a component in DepreciationLab, it calculates the remaining NBV, generates the derecognition journal, and recalculates the total depreciation schedule from the replacement date. No manual rework of the asset register required.

7. Component Method vs Single Asset: The P&L Impact {#pl-impact}

The financial statement impact of componentisation goes beyond the annual depreciation charge. Three effects compound over the asset's life.

Effect 1: Higher early depreciation. The component method front-loads more of the total cost into the first decade through short-lived components (fit-out, HVAC). This produces lower profits in early years for the same operating performance. For entities reporting against earnings targets or debt covenants with EBITDA or net income thresholds, this is not a neutral observation.

Effect 2: P&L spikes at component replacement. As sections above show, replacing a component before its estimated life ends produces a loss in the year of replacement. Single-asset accounting does not produce this spike: the replacement is simply capitalised or expensed as maintenance. The spike in component accounting is more accurate; it reflects an estimate revision. But it creates volatility that management needs to anticipate.

Effect 3: Lower balance sheet carrying amount. The component method produces higher cumulative depreciation in the early years. Net carrying amount is lower. For entities where PPE is a significant balance: GCC property developers, manufacturing groups, hotel operators: this affects leverage ratios, book value metrics, and return on assets calculations.

Comparison table: Years 1-10:

| Year | Component Method (USD) | Single Asset (USD) | Difference |

|---|---|---|---|

| 1-10 annual charge | 238,333 | 125,000 | +113,333 |

| Cumulative depreciation Year 10 | 2,383,330 | 1,250,000 | +1,133,330 |

| Net book value Year 10 | 2,616,670 | 3,750,000 | -1,133,330 |

At Year 10, the component method balance sheet shows a USD 2.6M building. The single-asset approach shows USD 3.75M. Both describe the same building. The difference is a USD 1.1M overstatement in the non-compliant approach.

8. IAS 16 Disclosure Requirements {#disclosure}

IAS 16.73 requires the following disclosures for each class of PPE:

- The measurement bases used (cost model or revaluation model)

- The depreciation methods used

- The useful lives or depreciation rates used

- The gross carrying amount and accumulated depreciation at the beginning and end of the period

- A reconciliation of the carrying amount from beginning to end of period

For componentised assets, the notes should identify:

- The significant components and their respective useful lives

- The depreciation method applied to each component

- Any component-level changes in estimates during the period, including the financial effect

IAS 8 implications for estimate changes: A revision to a component's estimated useful life is a change in accounting estimate under IAS 8.32. Apply prospectively. Disclose the nature of the change and, if practicable, the amount by which each line item in the financial statements is affected in the current period and future periods.

When componentisation is first applied to an existing asset: If this is a voluntary change in accounting policy, IAS 8.19 requires retrospective application with restatement of prior periods where practicable. If prior cost data is not available for retrospective allocation, use a current professional valuation as the best estimate of fair values at acquisition date.

9. Common Mistakes and Audit Findings in GCC Practice {#mistakes}

Component accounting is well-known. The mistakes are systematic: the same errors appear across entities in Bahrain, Saudi Arabia, and the UAE, year after year.

Mistake 1: Single life for the whole building. The classic non-compliance. A USD 40M hotel is depreciated at 40 years with a single schedule. No component breakdown. Auditors flag it. Management responds with a retroactive componentisation exercise that creates volatility in the current-year P&L as years of under-depreciation are corrected.

The fix is not retroactive cleanup. The fix is getting the initial componentisation right at acquisition.

Mistake 2: Capitalising replacements without derecognising the old component. The building's HVAC is replaced. The new system is capitalised. The old system remains on the asset register. Gross cost rises, accumulated depreciation is understated, and the asset is overstated. Every subsequent year, depreciation is calculated on a base that includes a fully replaced component.

Any significant replacement should trigger a derecognition assessment: is this a replacement of an existing significant component? If yes, remove the old carrying amount before capitalising the new one.

Mistake 3: Using one method for all components. IAS 16.62 permits different methods for different components. Where a process component's wear is usage-driven, units of production may be the correct method for that component while the structural elements use straight-line. Applying straight-line uniformly because it is simpler is not automatically wrong: but it needs to be supportable as the method that best reflects each component's consumption pattern.

Mistake 4: No documented significance threshold. Auditors ask for the accounting policy that supports the componentisation decisions made. Without a documented threshold, every component boundary becomes a subjective discussion. Write the policy: "The entity treats any part of a PPE item as a significant component where its cost exceeds 10% of the total asset cost and its useful life differs materially from the overall asset life."

Mistake 5: Forgetting the residual component. After separating the significant components, the remainder of the asset: costs that do not belong to any named component: is itself a component. It must be depreciated. The depreciation basis is the total asset cost less the sum of individually identified component costs, over the useful life of the overall asset. Entities that focus on the identified components and forget to build a residual schedule understate depreciation.

Mistake 6: No annual review of component lives. IAS 16.61 requires annual review of useful life estimates. For building components, this means checking at each year end whether the remaining life estimate is still supportable. A fit-out component installed in Year 1 with a 10-year estimate should be assessed at Year 7: is the fit-out actually going to last three more years, or has it deteriorated faster? If the estimate changes materially, revise it prospectively and disclose.

FAQ {#faq}

What is component depreciation under IAS 16?

Component depreciation is the IAS 16 requirement to depreciate significant parts of an asset separately when those parts have materially different useful lives. Each significant component is tracked independently with its own cost allocation, useful life, and depreciation method. Total annual depreciation for the asset equals the sum of all component charges. IAS 16.43 makes this mandatory: not optional: where significant components with different lives exist.

How do you identify significant components for depreciation?

Most entities apply a policy threshold of 10-15% of total asset cost. A part must also have a materially different useful life from the overall asset to warrant separation. Document the threshold as an accounting policy. Components below the threshold are aggregated into a residual category, depreciated over the overall asset life. For buildings, common significant components are structure, roof, HVAC, lifts, and interior fit-out: each with a different replacement cycle.

Is component depreciation required for all assets under IFRS?

No. It applies only where an asset has significant parts with materially different useful lives. Most vehicles, computers, and office equipment do not require componentisation. The requirement is most commonly triggered by complex long-lived assets: commercial buildings, industrial plants, ships, aircraft, and infrastructure. Small or immaterial components may be aggregated. The judgement: and the documentation of that judgement: sits with the entity.

What happens when a component is replaced before the end of its useful life?

Derecognise the old component. Remove its original cost and accumulated depreciation from the register. Recognise any remaining NBV as a loss in profit or loss in the replacement period. Then capitalise the new component at cost and begin depreciating it over its own estimated useful life. Not derecognising the old component is one of the most common audit findings in PPE-heavy entities.

How does component depreciation affect deferred tax?

Component depreciation typically generates higher total book depreciation than a single-asset approach, particularly in early years. Where tax authorities use a single rate for the whole asset, total book depreciation exceeds tax depreciation in the periods when short-lived components (fit-out, HVAC) are being charged at full rates. This creates a deductible temporary difference and a deferred tax asset. When components are replaced and derecognised, the associated deferred tax is settled in the period of derecognition. Model the deferred tax explicitly for each component, not as a single blended rate for the whole asset.

Does component depreciation apply to investment property under IAS 40?

Only for investment property measured under the cost model. IAS 40 permits cost model or fair value model. Under the cost model, the asset is depreciated using IAS 16 principles: including componentisation where applicable. Under the fair value model, the asset is not depreciated at all (gains and losses go through P&L directly), so component accounting does not apply. Most GCC real estate investment entities elect the fair value model; those that do not must apply full IAS 16 depreciation including componentisation.

What are the disclosure requirements for component depreciation?

IAS 16.73 requires: depreciation method and useful lives for each class of PPE, gross carrying amount and accumulated depreciation at period start and end, and a movement reconciliation. For componentised assets, identify significant components and their respective lives in the notes. Disclose derecognitions and their P&L impact. Changes to component life estimates are changes in accounting estimates under IAS 8: disclose the nature of the change and its financial effect in the current and future periods.

Conclusion

The USD 113,333 annual gap between USD 125,000 and USD 238,333 on the Bahrain building is not an accounting choice you can make either way. The single-asset approach misrepresents the consumption of economic benefits from that property. The component method records what is actually happening: a fit-out wearing out in 10 years, HVAC in 15, the roof in 20.

Getting componentisation right at acquisition avoids the painful retroactive corrections that arise when auditors flag a non-compliant single-asset schedule five years into the asset's life. Document the significance threshold, build the schedule by component from day one, and build the derecognition process into your PPE procedures before the first replacement cycle arrives.

The IAS 16 standard is not ambiguous on this point. The component depreciation method is mandatory where significant components exist with different useful lives. The only question is whether your asset register is set up to handle it correctly.

DepreciationLab is built for component accounting.

Define your components, assign useful lives and methods, and DepreciationLab generates the full multi-component schedule, handles derecognition calculations when you replace a component, and produces the IAS 16.73 disclosure tables your auditors need. No more manual spreadsheet merges.

Start your component schedule at depreciationlab.org The free plan covers 10 assets across all 7 methods. Professional is $12 per month or $99 per year: a 150-asset register, bulk Excel upload, and audit workpapers.

Related Posts

- The Complete Guide to All 7 Depreciation Methods (Pillar Post)

- Straight-Line Depreciation: Formula, Example & IAS 16 Guide

- Units of Production Depreciation: Formula, Example & IAS 16 Guide

- Declining Balance Depreciation Under Companies Act 2013: WDV Method Explained

- Free Fixed Asset Depreciation Calculator (Excel)

Part of the FinDataPro Depreciation Methods Series. All examples use USD unless otherwise stated. IAS 16 references are to the 2024 consolidated version. GCC regulatory references are to CBB Rulebook (Bahrain) and CMA rules (Saudi Arabia). Tax treatment varies by jurisdiction: verify applicable rules before applying.

⚡Try It Yourself

Calculate component depreciation for each significant part with separate useful lives. Start free at Depreciation Lab →

Prashant Panchal is a Chartered Accountant (ACA) and Financial Modelling & Valuation Analyst (FMVA®) with 19 years of experience in finance, FP&A, and financial modelling across the GCC region. He is the founder of FinDataPro.

Discussion

Leave a Comment

Comments are moderated and appear once approved.