UAE Corporate Tax9% Rate, Taxable Persons, Free Zone Rules, and Accounting Entries

The UAE corporate tax filing deadline for the first year was 30 September 2024. The volume of late registrations and penalty waivers that followed was not a capacity problem. It was a classification problem: companies that assumed their free zone structure made them exempt, or that the AED 375,000 threshold made them irrelevant, were both wrong in ways that had material consequences.

ACA | FMVA® | 19 Years in Finance

Overview: Federal Decree-Law No. 47 of 2022

The UAE corporate tax is governed by Federal Decree-Law No. 47 of 2022 on the Taxation of Corporations and Businesses. It applies to financial years beginning on or after 1 June 2023. A company with a 31 December year-end entered the corporate tax net from 1 January 2024 for the financial year ending 31 December 2024 -- but a company with a 30 June year-end was in the tax from 1 July 2023.

The UAE corporate tax rate structure:

| Taxable income band | Rate |

|---|---|

| AED 0 to AED 375,000 | 0% |

| Above AED 375,000 | 9% |

| Free Zone Qualifying Income | 0% |

| Multinationals (Pillar Two / DMTT, from 1 Jan 2025) | 15% effective minimum |

The UAE rate is not a flat 9%. The first AED 375,000 (approximately USD 102,000) is taxed at 0% for all standard taxable persons. Only the excess is taxed at 9%. For a company with AED 1,000,000 of taxable income, the tax is 9% of AED 625,000 = AED 56,250, not 9% of AED 1,000,000.

Taxable Persons and Exempt Persons

Resident taxable persons: All juridical persons (companies, partnerships with legal personality) incorporated or registered in the UAE, and foreign juridical persons that are effectively managed and controlled from the UAE.

Natural persons: Individuals conducting business in the UAE with business revenue exceeding AED 1 million in a calendar year are subject to UAE corporate tax from 1 January 2024 onward.

Exempt persons (not taxable):

- UAE Federal and Emirate government entities and their wholly-owned subsidiaries designated as exempt

- UAE extractive businesses covered by existing Emirate-level oil and gas concession agreements

- Qualifying public benefit entities (charities, registered educational and healthcare institutions)

- Qualifying investment funds meeting prescribed conditions

- Public pension or social security funds

Exemption is not automatic for most categories. Entities must apply to the Federal Tax Authority (FTA) and receive formal recognition. A private company that assumes it is exempt because it is owned by a government entity is making a dangerous assumption: only specifically designated entities are exempt.

Free Zone Qualifying Persons

A Free Zone Qualifying Person (FZQP) can apply a 0% rate on Qualifying Income. This is not an exemption: the FZQP remains a taxable person who files a return and pays tax on non-qualifying income at 9%. The ring-fencing is income-by-income, not entity-by-entity.

To maintain FZQP status, all four conditions must be met in every tax period:

- Adequate substance: The entity must have adequate assets, adequate number of qualified full-time employees, and adequate operating expenditure in a Free Zone or UAE in relation to its core income-generating activities.

- Qualifying Activities: Income must derive from transactions with other Free Zone Persons, or from specified Qualifying Activities including manufacturing of goods, processing of goods, holding of shares and other securities, treasury and financing services to related parties, ship operations, fund management services, and others prescribed by the Minister.

- De minimis non-qualifying revenue: Revenue that does not qualify must not exceed 5% of total revenue or AED 5 million, whichever is lower. Breach of the de minimis threshold in any year means all income in that year is taxed at 9%.

- No standard taxable person election: An FZQP can elect to be treated as a standard taxable person (and thereby apply the 9% rate and AED 375,000 threshold). Once made, this election is irrevocable for 5 years.

Pillar Two: Large multinational enterprise groups with consolidated group revenue exceeding EUR 750 million in at least two of the four preceding financial years are subject to the UAE Domestic Minimum Top-up Tax (DMTT) from financial years starting on or after 1 January 2025. The DMTT applies to bring the effective tax rate on UAE income to a minimum of 15%, regardless of free zone status or qualifying income treatment.

Small Business Relief

Taxable persons with revenue not exceeding AED 3 million in the current and all prior tax periods ending on or before 31 December 2026 can elect for Small Business Relief. Under this election, the taxable person is treated as having zero taxable income for the period.

Small Business Relief is an election, not an automatic exemption. It must be made in the tax return. The revenue threshold is AED 3 million -- not profit, not taxable income. Revenue above AED 3 million in any prior period disqualifies the entity from the election even if the current period revenue is below the threshold.

Members of a Multinational Enterprise group are not eligible for Small Business Relief, regardless of their individual revenue.

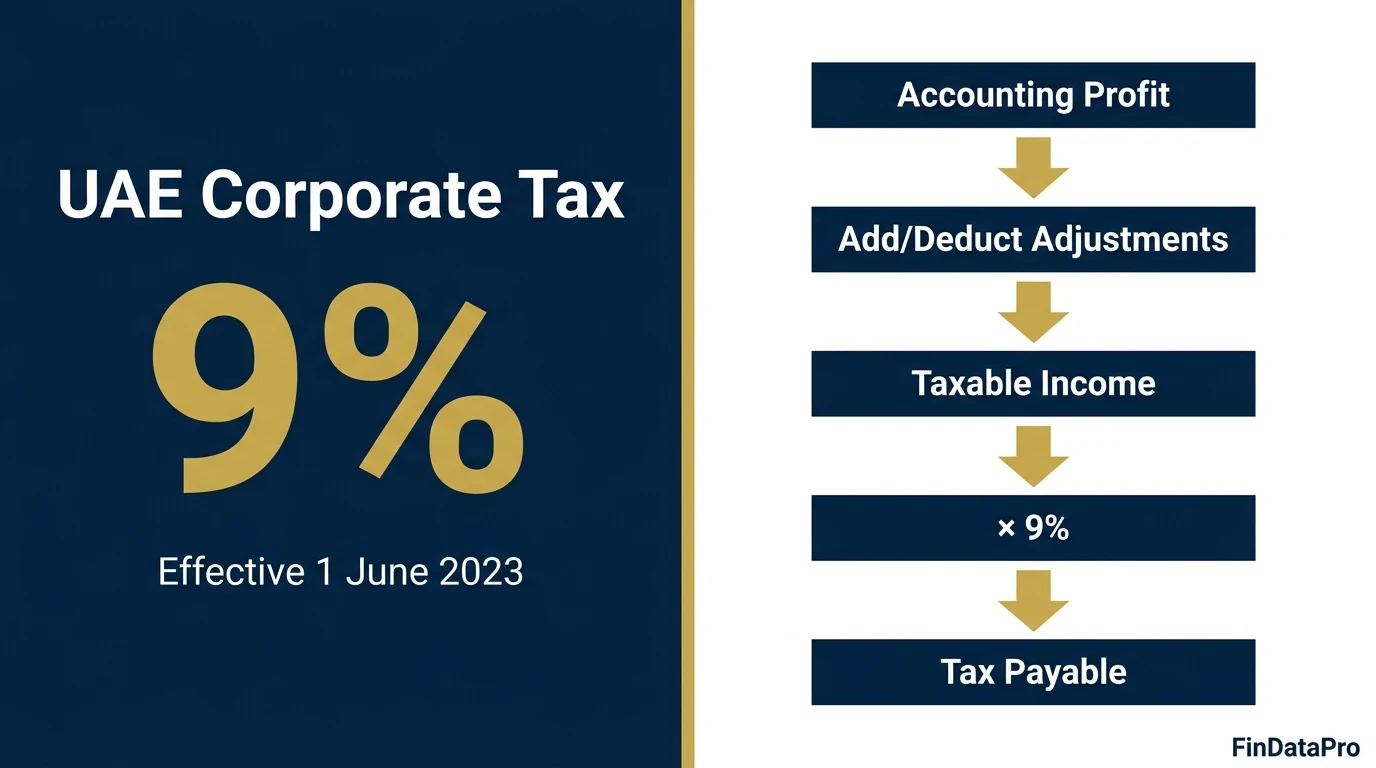

Calculating Taxable Income

Taxable income starts from the net profit or loss in the financial statements prepared under IFRS (or IFRS for SMEs, or another accounting standard accepted by the FTA for smaller entities). Adjustments are then made:

Taxable income calculation

Accounting net profit / (loss)

+ Non-deductible expenditure (fines, penalties, disallowed costs)

- Exempt income (qualifying dividends, qualifying capital gains)

+ Unrealised gains included in accounting profit (if realisation basis elected)

- Unrealised gains not yet taxable (if realisation basis elected)

+/- Other adjustments (related party adjustments, interest cap, etc.)

- Tax losses carried forward from prior periods

= Taxable Income

Participation exemption: Dividends received from UAE resident companies and capital gains on disposal of shares in UAE or foreign companies are exempt, provided the shareholding meets the participation conditions (generally 5% or more held for at least 12 months, and the subsidiary is subject to a corporate tax rate of at least 9% in its jurisdiction).

Realisation vs fair value: By default, the UAE corporate tax applies a realisation basis for unrealised gains and losses. A company can elect to apply a fair value basis for all assets and liabilities where fair value changes go through P&L. This election is irrevocable and applies to all such items.

Key Disallowable Deductions

| Disallowed item | Notes |

|---|---|

| Dividends and profit distributions to owners | These are equity distributions, not business expenses |

| Fines and penalties imposed by UAE authorities | Contractual penalties between private parties may be deductible |

| Bribes and illicit payments | Explicitly non-deductible |

| Personal expenses of owners | Must be wholly and exclusively for business |

| Expenses related to exempt income | Costs attributable to exempt dividend or capital gain income |

| Net interest expense above the cap (see below) | General Interest Limitation Rule applies |

| 50% of entertainment expenses (for non-qualifying purposes) | Only 50% of entertainment, amusement, and recreation costs are deductible |

Interest Limitation Rule

The General Interest Limitation Rule (GILR) limits the deduction of net interest expense to 30% of accounting EBITDA (earnings before interest, tax, depreciation, and amortisation as per the financial statements). If net interest expense exceeds 30% of EBITDA, the excess is disallowed but can be carried forward to future periods.

There is a safe harbour: if net interest expense does not exceed AED 12 million in the tax period, the limitation does not apply. For most small to medium UAE businesses, the AED 12 million safe harbour means the GILR is not a practical constraint. For GCC group treasury structures with significant intercompany lending, the 30% cap is material and requires modelling before the financial year end.

Accounting Entries

Under IAS 12, UAE corporate tax is accounted for using the current and deferred tax framework. Current tax is the tax payable based on the taxable income of the period. Deferred tax arises from temporary differences between carrying amounts and tax bases.

Current tax provision (year-end):

| Account | Dr | Cr |

|---|---|---|

| Current Tax Expense (P&L) | AED XXX | |

| Income Tax Payable (Balance Sheet) | AED XXX | |

| Recognise current year corporate tax liability at 9% of taxable income above AED 375,000 | ||

Payment of tax (within 9 months of year-end):

| Account | Dr | Cr |

|---|---|---|

| Income Tax Payable | AED XXX | |

| Cash / Bank | AED XXX |

Deferred Tax Under IAS 12

Prior to June 2023, most UAE entities had no deferred tax on their balance sheets because there was no corporate income tax. The introduction of UAE corporate tax triggered a first-time deferred tax recognition requirement for all temporary differences existing at the start of the first tax period.

Common sources of deferred tax under UAE corporate tax:

| Item | Accounting treatment | Tax treatment | Deferred tax |

|---|---|---|---|

| Property, plant and equipment (different depreciation lives) | Depreciated over useful life per IAS 16 | Depreciated per tax authority guidance | Liability if carrying amount > tax base |

| Doubtful debt provisions | Expensed when probable | Deductible only on write-off | Deferred tax asset |

| Unrealised fair value gains (realisation basis) | Recognised in P&L per IFRS 9 | Taxable on realisation | Deferred tax liability |

| Tax losses carried forward | Not recognised in accounting | Available to offset future taxable income | Deferred tax asset (if recovery probable) |

The deferred tax rate applied is 9% on all temporary differences attributable to standard taxable income. For FZQP entities, the rate applied to temporary differences on qualifying income is 0% -- which means no deferred tax is recognised on those differences.

Transfer Pricing

All transactions between related parties must be conducted at arm's length. The UAE adopts the OECD Transfer Pricing Guidelines as the standard. Related parties include persons connected through ownership (directly or indirectly, 50% or more) or control.

Transfer pricing documentation is required when the aggregate value of related party transactions exceeds AED 40 million in a financial year, or when the taxable person is required to file a Disclosure Form. A Master File and Local File must be prepared and ready for submission to the FTA upon request, within 30 days of a request being received.

Country-by-Country Reporting (CbCR) applies to UAE-headquartered Multinational Enterprise groups with consolidated group revenue exceeding AED 3.15 billion (approximately EUR 750 million) in the preceding financial year.

Registration and Filing Deadlines

All taxable persons -- including those who believe they will have zero taxable income or qualify for Small Business Relief -- must register with the Federal Tax Authority and obtain a Tax Registration Number (TRN) for corporate tax purposes. Non-registration is subject to a penalty of AED 10,000.

The registration deadline is generally within 3 months of the start of the first tax period, or within 3 months of the date the entity became a taxable person.

| Obligation | Deadline |

|---|---|

| Corporate tax registration | Within 3 months of start of first tax period (or as notified by FTA) |

| Annual tax return filing | Within 9 months after the end of the tax period |

| Tax payment | Within 9 months after the end of the tax period (same as return) |

| Transfer pricing documentation (Local File) | Within 30 days of FTA request |

Common Mistakes

Assuming free zone registration means tax exemption

Free zone status does not equal exemption. It provides potential access to a 0% rate on qualifying income, subject to meeting substance, activity, and de minimis conditions. Breach any one of these and all income is taxed at 9% for that year.

Not registering because taxable income is zero

Registration is compulsory regardless of income level, profitability, or exemption status. Zero taxable income does not eliminate the registration obligation. Penalty for failure: AED 10,000.

No deferred tax on balance sheet at transition

Entities that never recognised deferred tax under IAS 12 because there was no UAE income tax now have deferred tax obligations. The first IFRS financial statements covering a period subject to UAE corporate tax must recognise deferred tax on all material temporary differences at 9%.

Treating the AED 375,000 threshold as a flat exemption

The 0% band on the first AED 375,000 applies to all standard taxable persons. A company with AED 376,000 of taxable income pays 9% on AED 1,000 only, not on the full AED 376,000. Model the actual liability, not a simplification.

Ignoring transfer pricing documentation until requested

The 30-day response window for Local File production is not enough time to build documentation from scratch. If related party transactions exceed AED 40 million, the documentation must be prepared and maintained contemporaneously.

Frequently Asked Questions

What is the UAE corporate tax rate?

9% on taxable income above AED 375,000. The first AED 375,000 is taxed at 0%. Free Zone Qualifying Persons can apply 0% on qualifying income. The tax applies to financial years beginning on or after 1 June 2023.

Who is exempt from UAE corporate tax?

Exempt persons include UAE government entities and designated subsidiaries, UAE extractive businesses covered by existing concession agreements, qualifying public benefit entities, qualifying investment funds, and public pension funds. Exemption requires formal FTA recognition -- it is not automatic.

How are free zone companies taxed?

Free Zone Qualifying Persons pay 0% on qualifying income and 9% on non-qualifying income. To maintain FZQP status, they must meet substance requirements, derive income from qualifying activities, and keep non-qualifying revenue below the de minimis threshold. Multinationals with group revenue above EUR 750 million face a 15% minimum effective rate from 2025.

What is the Small Business Relief?

An election available to taxable persons with revenue below AED 3 million, treating them as having zero taxable income. Available for tax periods ending on or before 31 December 2026. Must be elected in the return -- not automatic. MNE group members are not eligible.

When is the UAE corporate tax return due?

Within 9 months after the end of the financial year. For a 31 December year-end: 30 September of the following year. Tax payment is due on the same date as the return. There is no advance payment requirement for most companies.

Related Posts

- IFRS 16 Lease Accounting: Right-of-Use Asset Guide (2026)

- SUMIFS Financial Analysis: Budget Variance and AR Aging

- Generative AI in Accounting: 2026 Implementation Guide

Official source: UAE Ministry of Finance: Corporate Tax.

Discussion

Leave a Comment

Comments are moderated and appear once approved.

Prashant Panchal is a Chartered Accountant (ACA) and Financial Modelling & Valuation Analyst (FMVA®) with 19 years of experience in finance, FP&A, and financial modelling across the GCC region. He is the founder of FinDataPro.