IFRS 16 Lease AccountingRight-of-Use Asset, Lease Liability, and Journal Entries

Most IFRS 16 errors in GCC companies are not technical. They are definitional: the arrangement is classified as a service contract, the calculation is never done, and the balance sheet carries zero where a lease liability should be. This guide covers lessee accounting from identification through to the full amortisation schedule and journal entries.

ACA | FMVA® | 19 Years in Finance

What Changed: IFRS 16 vs IAS 17

Under IAS 17, a lease was either a finance lease (on-balance-sheet) or an operating lease (off-balance-sheet). A decade of structured lease transactions specifically designed to qualify as operating leases made the distinction meaningless. IFRS 16, effective for periods starting on or after 1 January 2019, removed the classification test for lessees entirely.

Under IFRS 16 lease accounting, virtually all leases go on the balance sheet. The lessee recognises a right-of-use asset (what you have the right to use) and a lease liability (what you owe). Two narrow exemptions let you continue expensing: leases with a term of 12 months or less, and leases where the underlying asset is low-value. Everything else is on the balance sheet.

The income statement changes too. What was a single operating lease expense line becomes two separate charges: depreciation of the right-of-use asset (above EBIT) and interest on the lease liability (below EBIT). EBITDA goes up. Interest expense goes up. Net profit is the same over the lease term, but the timing and presentation differ.

Identifying a Lease Under IFRS 16

IFRS 16 defines a lease as a contract that conveys the right to control the use of an identified asset for a period of time in exchange for consideration. The three-part test is:

- Identified asset: Is there a specific asset identified in the contract? Supplier substitution rights matter here. If the supplier has a practical and economically beneficial right to substitute the asset throughout the period of use, there is no identified asset and no IFRS 16 lease.

- Substantially all economic benefits: Does the customer have the right to obtain substantially all the economic benefits from using the asset throughout the period of use?

- Right to direct use: Does the customer have the right to decide how and for what purpose the asset is used? Or was that already predetermined in the contract?

In GCC practice, the common misclassification is IT service contracts that include dedicated servers, fleet agreements where vehicles are assigned by registration number, and office equipment rentals where the supplier has no meaningful substitution right in practice. All three typically contain leases under IFRS 16 and require the calculation.

Practical Expedients: When You Can Skip the Calculation

IFRS 16 permits two recognition exemptions. If either applies, lease payments are expensed on a straight-line basis and no right-of-use asset or lease liability is recognised.

| Exemption | Condition | Note |

|---|---|---|

| Short-term lease | Lease term 12 months or less at commencement (including renewal options) | Applied by class of underlying asset |

| Low-value asset | Underlying asset worth less than approximately USD 5,000 when new | Applied on a lease-by-lease basis; assessed when the asset is new |

Low-value examples from IASB guidance: tablets, personal computers, small office furniture, telephones. A lease of a car is not low-value even if the monthly payments are modest. The test is the value of the underlying asset when new, not the lease payments.

Determining the Lease Term

The lease term for IFRS 16 purposes is the non-cancellable period plus optional extension periods that are reasonably certain to be exercised, and minus optional termination periods that are reasonably certain not to be exercised.

"Reasonably certain" is a high threshold. It is more than "more likely than not." Economic incentives matter: the lower the cost of not renewing (no significant leasehold improvements, no specialised location, easy relocation), the harder it is to justify including optional extension periods in the lease term. In GCC practice, five-year office leases with an option to renew for a further five years are often recognised with only the initial five-year term unless there is clear evidence of economic compulsion to renew.

The lease term assessment must be revisited when a significant event or change in circumstances occurs that is within the lessee's control, including the exercise or non-exercise of a renewal option.

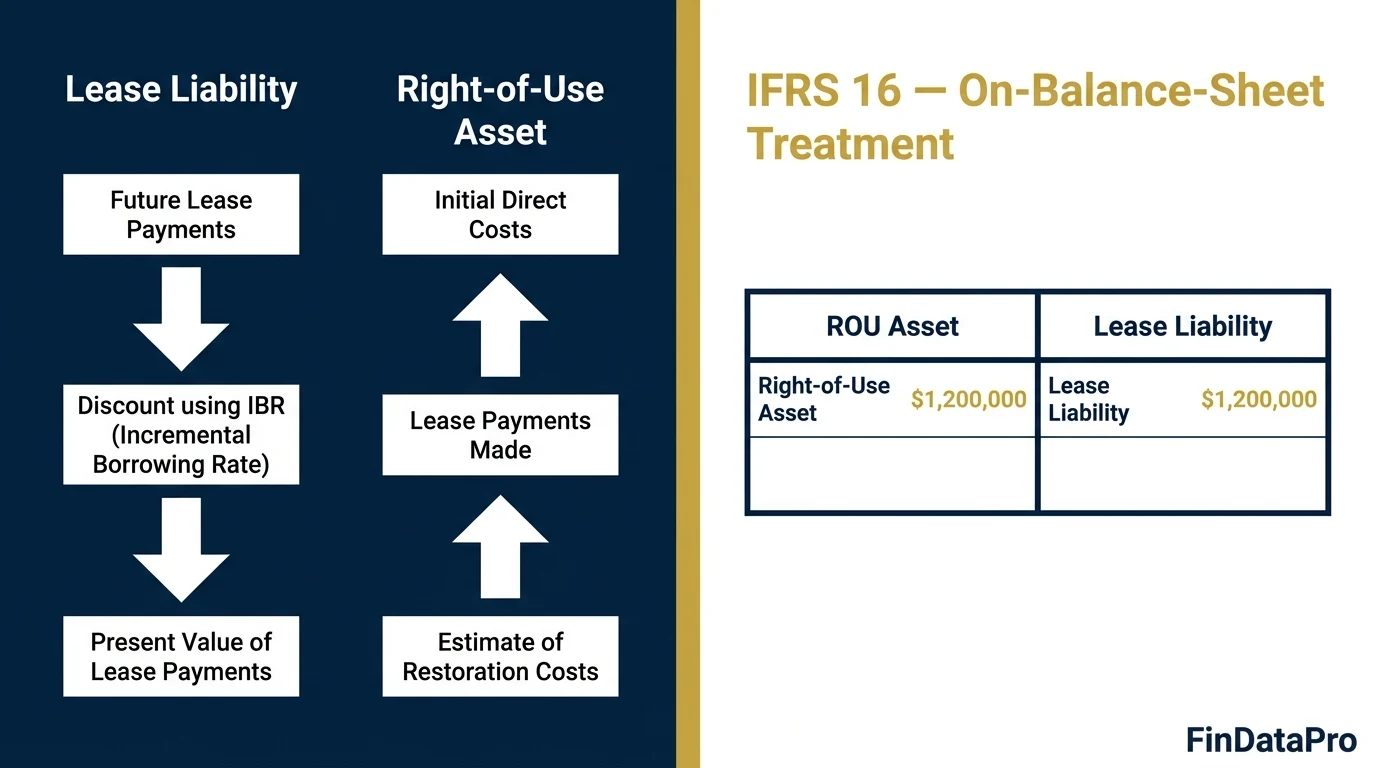

Lease Liability: Initial Measurement

The lease liability at commencement is the present value of the following payments over the lease term, discounted at the rate implicit in the lease or, if that cannot be readily determined, the lessee's incremental borrowing rate (IBR):

- Fixed payments, less any lease incentives receivable

- Variable lease payments that depend on an index or rate (using the index or rate at commencement date)

- Amounts expected to be payable under residual value guarantees

- Exercise price of a purchase option, if the lessee is reasonably certain to exercise it

- Payments of penalties for terminating the lease, if the lease term reflects the lessee exercising an early termination option

The rate implicit in the lease is the rate that causes the present value of the lease payments and the unguaranteed residual value to equal the fair value of the underlying asset plus initial direct costs of the lessor. In practice, lessees rarely have access to the lessor's residual value assumptions, so the IBR is used in the vast majority of IFRS 16 calculations.

The IBR reflects: the currency of the lease, the term of the lease, the nature and quality of the collateral (the right-of-use asset), and the economic environment. A BHD-denominated office lease in Bahrain for 5 years will use a different IBR than a USD-denominated equipment lease in Saudi Arabia for 3 years. The IBR is not the company's weighted average cost of capital.

Right-of-Use Asset: Initial Measurement

The right-of-use asset at commencement equals:

ROU Asset =

Initial lease liability

+ Lease payments made at or before commencement date (less incentives received)

+ Initial direct costs (legal fees, due diligence costs directly attributable to obtaining the lease)

+ Estimated dismantling / restoration costs (where an obligation exists under IAS 37)

In most GCC commercial property leases, initial direct costs are minimal and there is no dismantling obligation, so the ROU asset equals the lease liability plus any advance payments made before the commencement date.

Subsequent Measurement

Lease liability (after commencement): The liability increases each period by interest accrued at the IBR and decreases by lease payments made. This is the standard amortised cost method.

Right-of-use asset (after commencement): The ROU asset is depreciated on a straight-line basis over the shorter of the lease term and the useful life of the underlying asset, unless the lease transfers ownership or gives the lessee a purchase option that is reasonably certain to be exercised, in which case depreciation runs over the useful life of the asset. IAS 36 impairment testing applies to ROU assets in the same way as owned property, plant, and equipment. See the full straight-line depreciation guide for the mechanics of the SLN calculation.

The ROU asset and lease liability do not reduce by equal amounts in each period. Interest is highest in early periods (when the liability is largest) and falls over time. Depreciation of the ROU asset is equal each period (straight-line). As a result, the total charge to P&L is front-loaded compared to straight-line operating lease expense under IAS 17.

Worked Example: Office Lease in Bahrain

A company leases office space in Manama, Bahrain. Terms:

- Annual lease payment: BHD 12,000, paid in advance at the start of each year

- Lease term: 5 years, no renewal option exercised

- Incremental borrowing rate: 6% per annum

- No initial direct costs, no lease incentives, no dismantling obligation

- Commencement date: 1 January 2026

Step 1: Calculate the lease liability (PV of payments in advance)

Payments are made at the start of each year (annuity due). PV of annuity due at 6% for 5 years:

PV = Payment × [(1 - (1 + r)^-n) / r] × (1 + r)

PV = 12,000 × [(1 - (1.06)^-5) / 0.06] × 1.06

PV = 12,000 × 4.2124 × 1.06

PV = BHD 53,613 (rounded)Step 2: Right-of-use asset (= lease liability since no other additions)

ROU Asset = BHD 53,613

Step 3: Amortisation schedule (lease liability)

| Year | Opening liability (BHD) | Payment (BHD) | Interest @ 6% (BHD) | Closing liability (BHD) |

|---|---|---|---|---|

| 2026 | 53,613 | (12,000) | 2,496 | 44,109 |

| 2027 | 44,109 | (12,000) | 1,927 | 34,036 |

| 2028 | 34,036 | (12,000) | 1,322 | 23,358 |

| 2029 | 23,358 | (12,000) | 680 | 12,038 |

| 2030 | 12,038 | (12,000) | 2 | 40 |

Note: The BHD 40 rounding difference in Year 5 arises from rounding in the PV calculation. In practice, build the schedule to zero using the exact computed PV figure before rounding.

Step 4: ROU asset depreciation (straight-line over 5 years)

Annual depreciation = BHD 53,613 / 5 = BHD 10,723 per year.

Journal Entries

Commencement date (1 January 2026):

| Account | Dr (BHD) | Cr (BHD) |

|---|---|---|

| Right-of-Use Asset | 53,613 | |

| Lease Liability | 53,613 | |

| Recognise ROU asset and lease liability at PV of future payments | ||

First payment (1 January 2026, in advance):

| Account | Dr (BHD) | Cr (BHD) |

|---|---|---|

| Lease Liability | 12,000 | |

| Cash / Bank | 12,000 | |

| First annual payment reduces lease liability | ||

Year-end entries (31 December 2026):

| Account | Dr (BHD) | Cr (BHD) |

|---|---|---|

| Interest Expense (P&L) | 2,496 | |

| Lease Liability (interest accrual) | 2,496 | |

| Depreciation Expense (P&L) | 10,723 | |

| Accumulated Depreciation (ROU Asset) | 10,723 | |

| Year-end: accrue interest on lease liability; charge depreciation on ROU asset | ||

Total P&L charge in 2026: BHD 10,723 (depreciation) + BHD 2,496 (interest) = BHD 13,219. Under IAS 17 operating lease treatment, the charge would have been BHD 12,000 flat. The IFRS 16 front-loading effect: higher charge in early years, lower in later years, same total over the lease term.

GCC Context and Disclosure

IFRS 16 is mandatory for all entities applying full IFRS in the GCC. This includes listed companies in Saudi Arabia, Bahrain, UAE, Qatar, Kuwait, and Oman, as well as banks regulated by their respective central banks. The CBB (Central Bank of Bahrain) Rulebook requires financial institutions to follow IFRS as issued by the IASB, making IFRS 16 non-negotiable for Bahrain's banking sector.

Variable lease payments indexed to a local CPI (common in Saudi commercial leases) require reassessment of the lease liability when the index changes materially. The adjustment is made against the ROU asset, not through P&L.

Disclosure requirements under IFRS 16 are extensive. The notes must include: the depreciation charge for ROU assets by class, interest on lease liabilities, total cash outflow for leases, additions to ROU assets, a maturity analysis of lease liabilities, and short-term and low-value lease expense. Many first-time adopters underestimate the note disclosure burden.

For the full mechanics of right-of-use asset depreciation and when the component depreciation method under IAS 16 applies to ROU assets, see the component method guide. The complete depreciation methods guide covers all seven methods in one place.

Common Mistakes

Classifying IT service contracts as outside IFRS 16

Check whether the supplier has a genuine, practical right to substitute the asset. A data centre contract specifying a named server with no substitution right is a lease.

Using WACC as the incremental borrowing rate

The IBR is a borrowing rate, not a cost of capital rate. It should reflect the cost of secured borrowing with a similar term and in the same currency as the lease, not the overall cost of capital for the business.

Excluding optional renewal periods without assessment

The lease term includes extension periods that are reasonably certain to be exercised. If leasehold improvements are significant, relocation costs are high, or the location is economically irreplaceable, the extension period is likely in the lease term.

Treating the lease liability reduction as depreciation

The lease liability decreases by cash payments (less interest). The ROU asset decreases through depreciation. These are two separate entries that do not net off against each other. Confusing them produces a balance sheet that does not reconcile.

Missing the current / non-current split

The lease liability must be split between the portion due within 12 months (current) and the portion due after 12 months (non-current) in every balance sheet. The same applies to the accumulated depreciation presented against the ROU asset.

Frequently Asked Questions

What is the incremental borrowing rate (IBR) under IFRS 16?

The IBR is the rate a lessee would pay to borrow, over a similar term with similar security, the funds needed to obtain an equivalent asset in the same economic environment. It is the practical substitute for the rate implicit in the lease, which requires lessor data most lessees cannot access. The IBR varies by currency, lease term, and credit quality. A single company might use three different IBRs for three different leases running concurrently.

What is the difference between IFRS 16 and IAS 17?

IAS 17 split leases into operating (off-balance-sheet) and finance (on-balance-sheet). IFRS 16 abolished that split for lessees. All leases except short-term and low-value are now on the balance sheet. The lessor side of the standard remains largely unchanged: lessors still classify leases as operating or finance.

How do you calculate the lease liability under IFRS 16?

The lease liability is the present value of future lease payments not yet made, discounted at the rate implicit in the lease or the IBR. For an annuity due (payments in advance): PV = Payment × PV annuity factor × (1 + r). For an annuity in arrears (payments at end of period): PV = Payment × PV annuity factor. Build a period-by-period schedule: opening balance plus interest minus payment equals closing balance.

How is the right-of-use asset measured initially?

ROU Asset = initial lease liability + advance payments (less incentives received) + initial direct costs + estimated restoration costs. In most GCC commercial property leases, this simplifies to: lease liability plus any advance payment made at signing.

What are the practical expedients available under IFRS 16?

Two. First: short-term leases (12 months or less at commencement, including renewal options) can be expensed straight-line. Second: low-value asset leases (asset value below approximately USD 5,000 when new) can be expensed straight-line. Both can be applied independently on a lease-by-lease basis.

Related Posts

- 7 Depreciation Methods Every Accountant Must Know (2025)

- Component Depreciation Method: IAS 16 with Worked Examples

- Straight-Line Depreciation: Formula, Example and Excel (2025)

- Prepaid Expense Amortization Schedule Excel Template

IFRS 16 full text: IFRS Foundation — IFRS 16 Leases.

Discussion

Leave a Comment

Comments are moderated and appear once approved.

Prashant Panchal is a Chartered Accountant (ACA) and Financial Modelling & Valuation Analyst (FMVA®) with 19 years of experience in finance, FP&A, and financial modelling across the GCC region. He is the founder of FinDataPro.