WDV Depreciation Under Income Tax Act: Block of Assets and Section 32

Complete guide to WDV depreciation under Income Tax Act 1961. Block of assets, Section 32 rates, half-year rule, deferred tax impact, and worked examples for Indian CAs.

ACA | FMVA® | 19 Years in Finance

The block of assets concept is the most misunderstood mechanism in Indian tax depreciation: and the one that generates the most errors in tax returns, deferred tax calculations, and audit schedules. The misunderstanding is not about the rate. It is about the structure. Most Indian accountants know WDV depreciation runs at prescribed rates. Far fewer apply the block of assets logic correctly.

Here is the critical point: under the Income Tax Act 1961, WDV depreciation is not calculated on individual assets. It is calculated on a block of assets: a pool of all assets in the same class, at the same prescribed rate. When you add an asset to a block, its cost goes into the pool. When you sell one, the proceeds come off the pool. The block carries forward indefinitely until the last asset in it is disposed of.

If your tax depreciation workings show individual asset calculations under Section 32, they are wrong. Not technically different: wrong.

This matters beyond the tax return. The difference between Income Tax Act WDV and Companies Act WDV creates a deferred tax position under IAS 12 / Ind AS 12 that must be recognised every year. For entities with large fixed asset registers, that deferred tax balance is material, and it compounds if the block calculation is being done incorrectly.

Table of Contents {#toc}

- WDV Depreciation Under the Income Tax Act: Section 32

- Block of Assets: How It Works

- Prescribed Depreciation Rates

- The Half-Year Rule

- Step-by-Step Worked Example

- When You Sell an Asset: Balancing Charge and Terminal Depreciation

- Companies Act vs Income Tax Act WDV: The Structural Difference

- Deferred Tax: Why Both Calculations Must Run in Parallel

- Frequently Asked Questions

- Conclusion

WDV Depreciation Under the Income Tax Act: Section 32 {#section-32}

Section 32 of the Income Tax Act 1961 governs depreciation for income tax purposes. It allows a deduction for depreciation of assets used for the purpose of the business or profession. The deduction is available on a WDV basis at prescribed rates for each block of assets.

Key points from Section 32:

- Depreciation is mandatory, not optional. Even if the assessee does not claim it, the WDV is reduced by the notional depreciation amount, affecting the block's future years

- Only assets "used for the purpose of business or profession" during the previous year qualify

- An asset must be "owned" by the assessee: leased-in assets do not qualify (though finance lease assets may, depending on the nature of the lease)

- Assets used only for part of the year are subject to the half-year rule if acquired after 30 September

The authority reference: incometaxindia.gov.in publishes the current Section 32 rates and the Appendix I table of depreciation rates.

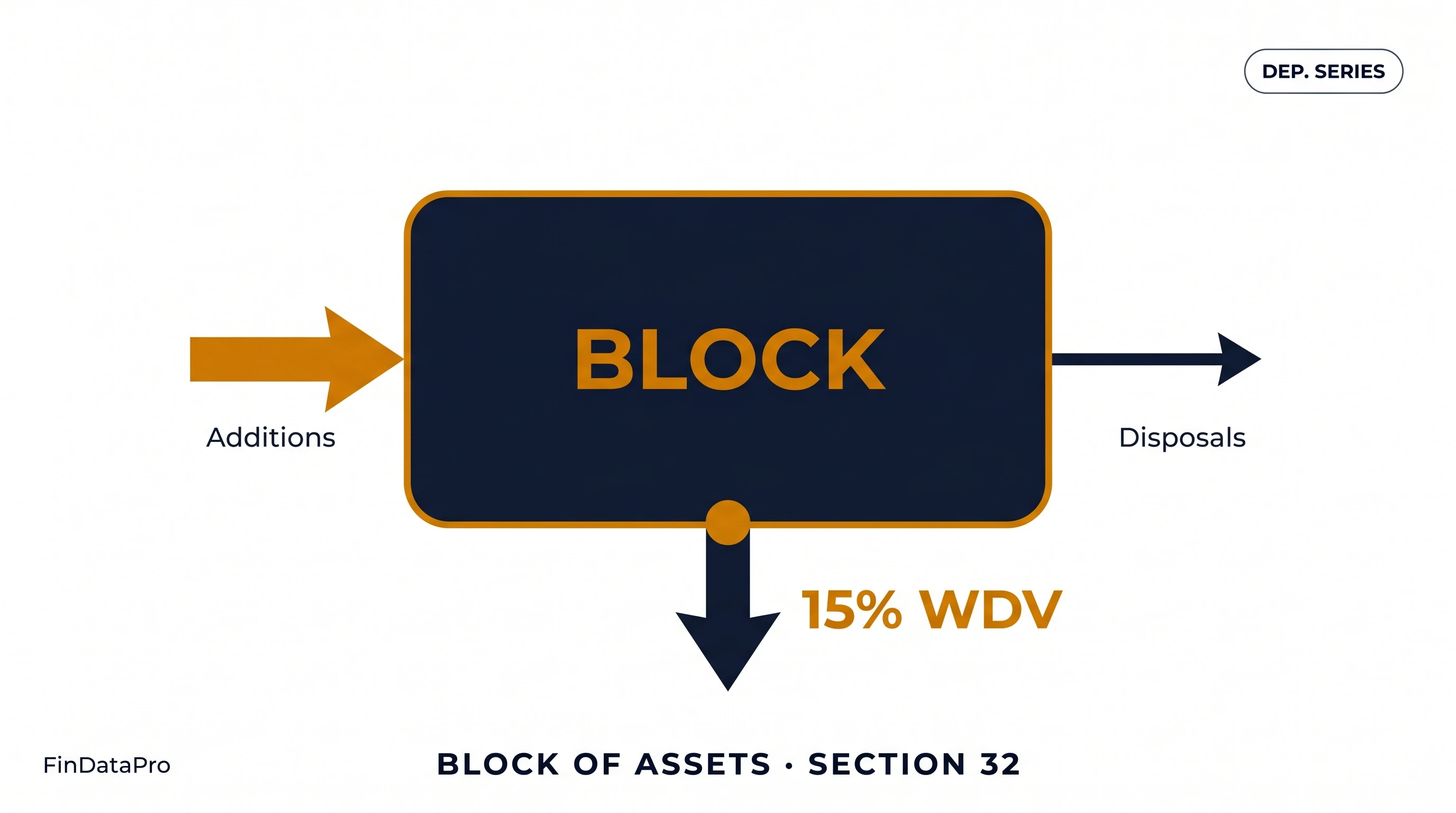

Block of Assets: How It Works {#block-of-assets}

A block of assets is a group comprising all assets falling within a class of assets for which the same prescribed depreciation rate applies.

The block WDV calculation:

WDV of Block = Opening WDV + Additions during the year - Sale proceeds of assets disposed of during the year

Depreciation is then applied to this net WDV at the prescribed rate.

Critical structural points:

Individual asset tracking ends at the block level. You cannot calculate depreciation on Machine A at 15% and Machine B at 15% separately and add them up. Both machines are in the same block. The block gets one WDV. The block gets one depreciation calculation. If you retire Machine A after 3 years, the sale proceeds reduce the block WDV. Machine B carries on in the same block.

The block never disappears during active use. Even if you sell all but one asset in the block, the block continues. It only ceases to exist when the last asset in the block is sold and the block WDV is either extinguished (balancing charge) or claimed (terminal depreciation).

Opening WDV for the first year. The WDV of a newly created block is zero until the first asset is added. The cost of the first asset creates the block's WDV. For assets acquired in subsequent years, additions are made to the existing block WDV.

Asset class definitions. The Income Tax Act specifies asset classes: buildings, furniture and fittings, plant and machinery (with various sub-categories), ships, aircraft, and intangible assets. An asset can belong to only one block based on its class and the applicable rate. Some assets within the same physical category carry different rates: computers at 40%, general plant and machinery at 15%: and must be maintained in separate blocks.

Prescribed Depreciation Rates {#prescribed-rates}

The following rates are from Appendix I of the Income Tax Rules. These are the rates commonly applied. Always verify current rates at incometaxindia.gov.in as legislative amendments can affect the applicable rates.

| Asset Class | Description | Rate |

|---|---|---|

| Buildings | Residential premises | 5% |

| Buildings | Other buildings (commercial, industrial) | 10% |

| Furniture and Fittings | General furniture and fittings | 10% |

| Plant and Machinery | General plant and machinery not otherwise specified | 15% |

| Plant and Machinery | Ocean-going ships | 20% |

| Plant and Machinery | Motor vehicles (not used in hire business) | 15% |

| Plant and Machinery | Motor taxis, motor buses, motor lorries (hire) | 30% |

| Plant and Machinery | Computers and computer software | 40% |

| Plant and Machinery | Energy saving devices | 40% |

| Intangible Assets | Know-how, patents, copyrights, trademarks | 25% |

Note on intangible assets: The Finance Act 2021 inserted an amendment restricting WDV depreciation on self-generated intangibles and goodwill. Verify the current position with a tax advisor for goodwill acquired in business combinations.

The Half-Year Rule {#half-year-rule}

Assets acquired and put to use for less than 180 days during the previous year: that is, acquired after 30 September in the Indian financial year running from 1 April to 31 March: are eligible for only 50% of the standard depreciation rate in Year 1.

How it applies:

An asset added to the Plant and Machinery block (15% rate) on 1 October or later gets 7.5% in Year 1 (50% of 15%). From Year 2 onwards, the standard 15% rate applies to the block WDV.

The calculation in practice:

When a block has both full-year assets and half-year assets added in the same year, the WDV calculation must separate the two:

| Component | Amount (INR) |

|---|---|

| Opening WDV of block | 800,000 |

| Additions before 30 September (full-year eligible) | 200,000 |

| Additions after 30 September (half-year rule applies) | 100,000 |

| Depreciation on opening WDV + full-year additions: (800,000 + 200,000) × 15% | (150,000) |

| Depreciation on half-year additions: 100,000 × 7.5% | (7,500) |

| Total depreciation | (157,500) |

| Closing WDV | 942,500 |

This is not an optional calculation split. The Income Tax Act specifically requires the 50% restriction for additions in the second half of the year, and the assessment officer will apply it even if the assessee has not.

Step-by-Step Worked Example {#worked-example}

Block: Plant and Machinery (15% rate)

Year data:

| Item | Amount (INR) |

|---|---|

| Opening WDV of block (1 April) | 800,000 |

| Addition: machine purchased 1 June (full year) | 200,000 |

| Disposal: sale proceeds of one machine | (50,000) |

| WDV for depreciation: 800,000 + 200,000 - 50,000 | 950,000 |

| Depreciation at 15% | (142,500) |

| Closing WDV (31 March) | 807,500 |

Year 2: carrying the block forward:

| Item | Amount (INR) |

|---|---|

| Opening WDV (prior closing WDV) | 807,500 |

| No additions, no disposals | : |

| WDV for depreciation | 807,500 |

| Depreciation at 15% | (121,125) |

| Closing WDV | 686,375 |

The block never reaches zero unless all assets in it are sold. The WDV declines each year but never hits zero as long as one asset remains in service.

When You Sell an Asset: Balancing Charge and Terminal Depreciation {#disposal}

Normal disposal: block continues:

Sale proceeds reduce the block WDV. Depreciation continues on the remaining block in subsequent years. No separate gain or loss calculation is required at the individual asset level: the block absorbs the disposal.

Disposal where proceeds exceed block WDV (balancing charge):

If total sale proceeds from disposed assets exceed the WDV of the block, the difference is a balancing charge: taxable income in the year of disposal.

Balancing Charge = Sale Proceeds - Block WDV (if positive)

This is added to income and taxed at the applicable rate. It commonly occurs when a business sells assets with higher market values than their depreciated block WDV, particularly for technology assets that retained market value despite high tax depreciation rates.

Disposal of all assets: terminal depreciation:

When all assets in a block are sold and the block WDV exceeds the sale proceeds, the remaining positive WDV is terminal depreciation: an additional deduction claimed in the year the block is emptied.

Terminal Depreciation = Block WDV - Sale Proceeds (if WDV > proceeds)

This provision ensures that if the total depreciation claimed plus the sale proceeds is less than the original cost, the remaining unrecovered cost is deductible.

Companies Act vs Income Tax Act WDV: The Structural Difference {#comparison}

The same asset. The same rate name (WDV). Completely different calculations.

| Feature | Companies Act 2013 | Income Tax Act 1961 |

|---|---|---|

| Basis | Useful life (Schedule II) → derive rate | Prescribed rate directly (Section 32) |

| Unit of calculation | Individual asset | Block of assets (group) |

| Residual value | 5% default (mandatory) | None |

| Rate determination | 1 - (Residual/Cost)^(1/Life) | Table lookup: fixed rate |

| Partial year assets | Proportionate by months | 50% restriction if after 30 September |

| Asset disposal | Asset derecognised individually | Proceeds reduce block WDV |

| End of life | Asset reaches 5% residual, stops | Block never hits zero while assets remain |

| Applicable to financials | Yes (Companies Act compliance) | No (tax return only) |

Run both in parallel. They will always produce different numbers.

Deferred Tax: Why Both Calculations Must Run in Parallel {#deferred-tax}

Every Indian entity with fixed assets has two depreciation numbers: the Companies Act number (book depreciation) and the Income Tax Act number (tax depreciation). The difference between them is a timing difference under Ind AS 12 / IAS 12. That difference must be recognised as deferred tax on the balance sheet.

How the deferred tax builds:

In the early years of an asset's life, tax depreciation (at prescribed rates like 15% or 40%) typically exceeds book depreciation (derived from Schedule II useful lives and individual asset calculation). The excess creates a deferred tax liability: you are getting the benefit of lower tax now but will pay more tax in later years when book depreciation continues but the tax base is already low.

A simplified illustration:

Plant and Machinery. Cost: INR 1,000,000. Companies Act: 25.89% WDV (10-year life, 5% residual). Income Tax: 15% WDV block rate.

| Year | Book Depreciation (CA) INR | Tax Depreciation (ITA) INR | Timing Difference INR | Deferred Tax @ 30% INR |

|---|---|---|---|---|

| 1 | 258,900 | 150,000 | 108,900 DTA | 32,670 DTA |

| 2 | 191,916 | 127,500 | 64,416 DTA | 19,325 DTA |

| 3 | 142,259 | 108,375 | 33,884 DTA | 10,165 DTA |

In this example, book depreciation exceeds tax depreciation in early years (because the Companies Act WDV rate of 25.89% is higher than the Income Tax rate of 15%), creating a deferred tax asset. The direction of the timing difference depends on which rate is higher: it varies by asset class.

The critical point: if you are only maintaining one depreciation schedule and treating it as both the book and tax figure, you are not complying with Ind AS 12. You are also producing an incomplete balance sheet.

Building and maintaining parallel depreciation schedules: Companies Act WDV for each individual asset and Income Tax Act WDV for each block: across a register of 50 or more assets is where manual errors accumulate the fastest. The block calculation alone requires tracking additions, disposals, and half-year adjustments across multiple asset classes simultaneously.

DepreciationLab runs both calculations in parallel: Companies Act individual asset WDV and Income Tax Act block-of-assets WDV, with the deferred tax position computed automatically from the timing difference. Built for Indian CAs and finance managers who need both schedules to be right without maintaining two separate Excel models. Try DepreciationLab at depreciationlab.org.

Frequently Asked Questions {#faq}

What is WDV depreciation under the Income Tax Act 1961?

WDV (Written Down Value) depreciation under the Income Tax Act is the system for claiming tax depreciation under Section 32. Prescribed rates are applied to the written-down value of a block of assets: not individual assets. The block continues to carry forward until all assets in it are disposed of. The full rates are published at incometaxindia.gov.in.

What is the block of assets concept in Indian tax depreciation?

A block of assets is a pool of all assets of the same class with the same prescribed depreciation rate. General plant and machinery at 15% forms one block. Computers at 40% form a separate block. Depreciation is computed on the block as a whole. Individual asset tracking within the block is not required for the tax calculation: only the block WDV matters.

What are the WDV depreciation rates under the Income Tax Act?

Key rates: Buildings residential 5%, commercial 10%, furniture 10%, plant and machinery (general) 15%, motor vehicles 15%, computers and software 40%, ships 20%, intangible assets 25%. Full current rates at incometaxindia.gov.in.

What is the half-year rule for Income Tax depreciation?

Assets put to use for less than 180 days: acquired after 30 September: attract only 50% of the standard rate in Year 1. Full-year rate applies from Year 2. The two types of additions (before and after 30 September) must be tracked separately for the first year calculation.

What happens when you sell an asset from a block?

Sale proceeds reduce the block WDV. Depreciation continues on the remaining block. If proceeds exceed the block WDV: balancing charge (taxable income). If all assets in the block are sold and WDV exceeds proceeds: terminal depreciation deduction.

What is the difference between WDV under Companies Act and Income Tax Act?

Completely different structures. Companies Act: individual assets, rate derived from useful life, 5% residual value. Income Tax Act: block of assets, prescribed rate from table, no residual value. They will always produce different depreciation numbers for the same assets.

How does Income Tax depreciation create deferred tax in Indian companies?

The difference between tax depreciation (Income Tax Act) and book depreciation (Companies Act) is a timing difference under Ind AS 12. Deferred tax liability arises when tax depreciation exceeds book. Deferred tax asset arises when book exceeds tax. Both must be recognised on the balance sheet every reporting period.

Is there a residual value under Income Tax Act WDV?

No. The Income Tax Act does not incorporate a residual value into the WDV calculation. The block WDV continues to decline at the prescribed rate indefinitely until the block is emptied by disposal. This contrasts directly with the Companies Act method, which stops at the 5% residual value.

Conclusion {#conclusion}

WDV depreciation under the Income Tax Act is not a simplified version of Companies Act WDV. It is a structurally different calculation built on a pool-based logic that most individual-asset depreciation schedules cannot replicate correctly.

The block of assets concept eliminates individual asset tracking for tax purposes, creates a perpetual pool that survives individual disposals, and generates timing differences against book depreciation that must be recognised as deferred tax every year.

For Indian entities with significant fixed asset registers: multiple blocks, mixed acquisition dates, disposals, and the half-year rule to manage: maintaining two parallel depreciation calculations manually in Excel is the approach that generates the most errors at year-end.

DepreciationLab handles Companies Act WDV and Income Tax Act block-of-assets WDV simultaneously, producing both schedules from a single asset register entry. No separate models. No manual reconciliation.

Try DepreciationLab Free → The free plan covers 10 assets across all 7 methods. Professional is $12 per month or $99 per year: a 150-asset register, bulk Excel upload, and audit workpapers.

Part of the FinDataPro Depreciation Methods Series. Related posts:

- The Complete Guide to All 7 Depreciation Methods (Pillar)

- WDV Depreciation: Companies Act 2013: Schedule II and Rates

- Straight-Line Depreciation: Formula, Example and Excel

- Free Fixed Asset Depreciation Calculator (Excel)

⚡Try It Yourself

Calculate WDV depreciation under Indian Income Tax Act with block of assets support. Start free at Depreciation Lab →

Prashant Panchal is a Chartered Accountant (ACA) and Financial Modelling & Valuation Analyst (FMVA®) with 19 years of experience in finance, FP&A, and financial modelling across the GCC region. He is the founder of FinDataPro.

Discussion

Leave a Comment

Comments are moderated and appear once approved.